05/31/2024 by +K2N Tax Team 0 Comments

Estimated Taxes - Why pay them and how to Avoid Penalties

Estimated tax penalties - a nuisance and sometimes unwelcome surprise.

Predicting what we will owe each year before the year is complete can be complicated, and sometimes it can seem unfair to owe penalty on taxes that are not really due yet, however the authority has been granted to to the IRS to make sure we are paying tax obligations throughout the year, which is basically a normal process for most employed individuals.

The estimated tax process is designed to have the same "throughout the year" effect.

Why Do I owe Estimated Taxes?

Most taxpayers owe estimated tax payments when they:

- Paid estimates in the prior year to cover tax.

- Had a balance due for the prior year.

- Project that their taxes withheld will not cover a certain percentage of the prior year tax.

Are Estimated Tax Payments Required?

Payments are required to reduce or eliminate underpayment penalties, however these amounts are not considered due for IRS collection purposes until the statutory deadline for paying tax (normally April 15 for individual filers). The minimum threshold for estimated tax is $1,000 federally and varies by state.

How Much Should I Pay?

Federally, there are two safe-harbors which can help you to avoid potential penalties, so long as you pay enough to cover your tax obligation (estimates, withholdings and other payments):

- 100% (110% if AGI>$150,000 ) of the prior year tax

- 90% of the current year tax

*If your income is significantly variable throughout the year, or if you have specific circumstances where a one time income event occurs during the you may qualify for a different schedule using “annualization” or “seasonal” installments

How are the Penalties Calculated?

First determine your balance due without respect to estimates paid. In most cases, 25% is due each quarter… and the penalty must actually be computed separately for each quarter.

The penalty is a function of rate/365, published quarterly and multiplied by the 25% amount and again by the number of “late days.”

e.g. Assume only withholdings were paid during the year & a $1,000 balance is due by April 15, 2024 (day 366 per IRS tables), simply subtract the quarterly due date from the payment date, to calculate the “late days.”

- Apr 15, 2023 is day 0 and 366 days late

- Jun 15 is day 61 is 305 days late

- Sept 15 is day 153 is 213 days late

- Jan 15, 2024 is day 275 is 91 days late

Penalty calculates to $48.82 as follows:

- Q1 $250 x .07/365 x 366 = 17.54

- Q2 $250 x .07/365 x 305 = 14.62

- Q3 $250 x .08/365 x 213 = 11.67

- Q4 $250 x .08/365 x 91 = 4.99

What about State Estimates?

Each state has their own rules around estimates and you should check with your state revenue agency, however in most cases, interest rates are slightly higher (normally +1%) and the amount is

Additional Resources for State information regarding estimated taxes

Can I Pay Electronically?

Most agencies encourage electronic payment and will keep a history for you. We recommend that you retain your receipts and verify your bank records to confirm your payments clear. Below are a few local state resources.

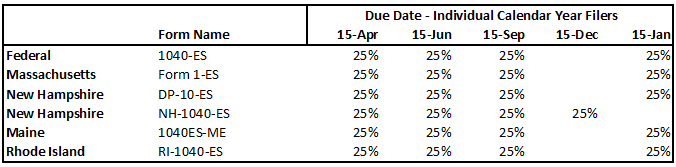

When Are Payments Due?

In most cases for calendar year individuals, your payments are due on the 15th of the April, June, September and January (of the following year). However, some states have due dates requiring a December payment, such as New Hampshire for business related taxes.

Links to Resources Related to Estimates

Internal Revenue Service

IRS Tax Payments

New Hampshire Interest & Dividends Tax

New Hampshire Business Tax

Granite Tax Connect

Connecticut CT-1040ES

MyConneCT

Rhode Island RI-1040ES

RI Online Payments

Comments